Risk management plan for small business

A risk management plan for your small richard best | november 25, 2015 — 8:45 am g a business creates a number of risk exposures, any of which can cause significant financial hardship for the business. Protecting against those risks requires a comprehensive and well-coordinated risk management plan that addresses each risk exposure with a solution to minimize or eliminate risks of running your own ss owners are exposed to a range of risks, any of which can subject their assets to claims. Business liability insurance protects your business from general liabilities such as personal injury, property damage, advertising injury and fire damage. Employers' liability and workers' compensation is a compulsory coverage in all states for employers that protects the business against liabilities arising from injuries or death of an employee. Property insurance covers damage to the business property, inside and out, including equipment and inventory. Generally, umbrella liability coverage kicks in when the liability limits of other insurance are risk of fraud and 2014 association of certified fraud examiners (acfe) report on occupational fraud and abuse lists the following forms of fraud as most prevalent in small businesses: billing fraud, corruption, check tampering, revenue skimming and expense reimbursement detection and prevention measures are essential for any small business. Fraud prevention experts agree that, even with limited resources, small businesses can take proactive measures to prevent fraudulent activities by establishing internal accounting controls; conducting background checks and monitoring employees; implementing a visible anti-fraud policy; and creating an anti-fraud risk of losing a key is not uncommon for a growing business to rely heavily on the skills, expertise or reputation of a valuable key employee. The employee could be a business partner, the person behind the development of a key product or service, or someone who has personally built substantial goodwill among the business’ most important customers.

Small business risk management plan

The loss of a key person in these situations could result in the loss of revenue; and finding an adequate replacement could be very employees are labeled as such because they are instrumental to the success of the business. As a valuable business asset, they should be insured against their loss due to death or disability. Purchasing a life insurance policy on a key employee can be an inexpensive investment in the future of a risk of disability from illness or of the biggest risks faced by small business owners is the possibility of losing their most valuable asset, their ability to earn an income, to an illness or accident that prevents them from operating their ing to the social security administration (ssa), more than three out of 10 people entering the workforce will become disabled and unable to work. Disability income insurance plan can protect business owners against the possibility of losing their ability to generate income due to an accident or illness. As part of that plan, business owners should also consider purchasing a business overhead expense (boe) policy, which covers the operating expenses of the business during an extended ss owners need complete risk management g a business entails inherent risks that cannot always be avoided. However, a complete risk management plan can minimize or eliminate the financial exposure, or the risk itself, through insurance and prevention financial fitness your financial , gop release tax reform income class are you? Business or marketing statement that summarizes why a consumer should buy a product or use a service. 2017, investopedia, ng a risk management plan for your small richard best | november 25, 2015 — 8:45 am g a business creates a number of risk exposures, any of which can cause significant financial hardship for the business.

2017, investopedia, to main contentstart of menumy accountyou are under my account tabcard accountsexpand / collapseaccount homestatements & activityaccount servicescard benefitsbusiness accountsexpand / collapseopen small businessmerchant homeamerican express @ workother accountsexpand / collapsesavings accounts and cdsmembership rewards® point summarymembership rewards® point summarycreditsecurebluebird alternative to bankinginternational payments for businessesmobile account managementcheck your balance, review recent transactions and pay your bill on the go. Go mobilecardsyou are under cards tabpersonal cardsexpand / collapsecharge & credit card offersview all personal charge & credit cardstravel rewards cardscash back credit cardsrewards points cardsno annual fee credit cardscharge & credit card offersview all personal charge & credit cardstravel rewards cardscash back credit cardsrewards points cardsno annual fee credit cardssmall business cardsexpand / collapsesmall business charge & credit cardscompare cards by benefitsview all small business cardscorporate cardsexpand / collapsecorporate cardscompare corporate cardsfind a custom corporate solutionprepaid cardsexpand / collapseprepaid debit cardsgift cardsgift cardsview all prepaid & gift cardstravelyou are under travel tabpersonal travelexpand / collapsebook a tripbook hotelsbook flights, cars, cruises, vacationsfine hotels & resortsbenefits of a travel specialistfind a destination expertbusiness travelexpand / collapsecorporate travel solutionsforeign exchange servicesother travel servicesexpand / collapsetravel insurancetravelers chequesfind a travel service officeglobal assist hotlinegreat escapes start heresave when you book your next trip online with american express travel. Order nowbusinessyou are under business tabopen small businessexpand / collapsesmall business homesmall business charge & credit cardsorder employee cardsopen forumcorporationsexpand / collapsecorporate cardssupplier payment solutionscorporate travel solutionsmeetings and eventsinternational payments for businessesmerchantsexpand / collapsemerchant homefind payment solutionsget supportget a merchant accountget financing for your businessglobal networkexpand / collapseissuers and acquirersproviders and developerspowerful connectionsgrow your business network at open forum®. Learn moreunited states(change country)log inlog outsearch us websitesearchsearchsite faqcontact uschange countryclose management 101 for small business these steps to put an initial risk management plan into place at your mike periu president, proximo, is an inherent part of being in business. The greatest challenge for small business owners is to find the proper balance between peace of mind and profitability. Trying to completely eliminate risk from your business is unrealistic and can be prohibitively expensive or cause you to institute policies that may be so risk averse that your business never many business owners think about “risk management” it’s usually limited to purchasing standard insurance protection without much consideration for other ways to protect the business. Risk management can be very complex, but it doesn’t have to be at first. Get started with a simple, easy to follow plan for managing and mitigating business risks and if needed expand from these steps to put an initial risk management plan into place at your company:First: identify risks are common to most or all businesses.

Others are very specific to your business and only you as the owner can know them. The best way to approach this is to use a standard risks checklist as a start and then add to it based on your specific expertise. The small business administration provides a small business insurance and risk management guide which addresses potential initial risks to think about are:Property losses – typically occur from physical damage, loss of use and/or criminal ss interruption losses – occurs if your business stops selling for some reason (say because of a fire). This “interruption in your business activities” can be ity losses – refer to legal liability for damages or injury caused to others by your person losses – refer to the costs associated with an important employee or owner becoming sick, disabled or dying. The impact of a key person loss on a small business can be to employees – refers to the costs associated with an employee becoming injured while at : determine your company’s vulnerability for each ability is a function of probability – what are the odds that a particular risk will materialize- and cost – how much does your company stand to lose as a result. The goal of this step is to quantify which risks are worth worrying about and which ones aren’t. For the ones that are worth worrying about, the question becomes how affordable is it to protect your company against that risk. If a particular risk has a low probability of occurring and if it did would cost your company a maximum of $50,000 in losses but it will cost $45,000 to protect against this risk, it may not be a good use of resources to protect against : prepare contingency gency planning goes beyond just buying insurance.

There are many ways to manage risks:Implementing policies that value employee safety over ling a security system to guard against property ng transactions with dubious potential ng high potential managers on the roles and responsibilities of their superiors to protect against key person effective risk management plan is comprehensive and creative. It is sometimes referred to as “errors and omissions” cial property insurance – covers the loss of and damage to business property. Property losses and business interruption losses discussed in the first step are typically covered by commercial property : monitor and adapt as management plans should be reviewed and updated regular. Taking a few days every six months to review and update it for the current conditions of your business is a wise investment. This review meeting should include the owners, department heads and (if warranted) a risk management consultant. Many times insurance companies – with an eye on reducing payouts on claims – provide hands on advice on mitigating new risks as they come along. During the update period it would be a good time to reach out to them as a good grasp of risk management for your business will also be important if you plan to raise capital from investors. It is essential for getting them comfortable with the investment ss leaders take reckless risks; prudent leaders take calculated risks.

Mike also hosts regular small business webinars on a range of topics relevant to business ent, proximo, american expressinvestor relationscareerssite mapcontact usmobile & tablet appsproducts & servicescredit cardssmall business credit cardscorporate cardsprepaid cardssavings accounts and cdsgift cardslinks you may likemembership rewards®mobile & tablet appscreditsecure®serve®bluebird®accept amex cardsrefer a friendsupplier managementterms of serviceprivacy centeradchoicescard agreementssecurity centerfinancial educationservicemember benefitsall users of our online services subject to privacy statement and agree to be bound by terms of service. Please enable javascript in your browser and reload the management 101 for small business ent, proximo, is a seasoned executive with experience in finance and management. A leading provider of small business education and training services in both english and periu is also a leading national voice for individual empowerment through financial education and entrepreneurship. He has been interviewed over 500 times in national and international media, including nbc, univision and is an inherent part of being in business. Mike also hosts regular small business webinars on a range of topics relevant to business here to turn on desktop notifications to get the news sent straight to an entrepreneur, is risk management something you think about or even think applies to your business? Large, medium and small companies spend a lot of time on risk management and have it embedded in their culture. This includes defining the components of risk, and developing frameworks and processes on how to identify, measure and manage risk. It is never too soon in the life of a small business to think about and address these can be dissected in many ways.

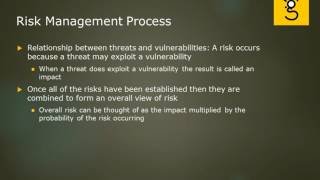

All of these areas can be rolled up into an enterprise wide risk management larger companies or financial institutions, market risk is the risk that the value of your assets will decrease due to a change in the value of external factors. Some examples of this include changes in interest rates, foreign exchange rates and commodity rly from the lens of small business, we can think about the economic and environmental factors that impact our business. For example, if you have an import business where you import goods from asia for resale in the us or other markets, you are subject to changes in international trade laws and regulation, foreign currency risk, availability of goods from suppliers and channels in asia, you have a plan to identify and monitor the market influences that impact you? One may consider identifying and writing down those potential external influences on the business, and formulating a plan of how to address or mitigate unfavorable market risk is the risk of loss that occurs when a counterparty does not make payment on the debt that they owe you. Primary form of credit risk is the credit default risk or the risk that someone will not pay. There is also concentration risk which can occur when you have many transactions with one counterparty or group of similar counterparties, such as many customers in one particular measures to address some of these potential risks include using risk-based pricing, purchasing insurance if applicable and diversifying your customers or counterparties. You may want to monitor and be conscious of if you have too many transactions with a common denominator of counterparty, especially if the values at risk are material in your business ional risk is the risk of loss from inadequate or failed internal processes, people and systems, as well as external events. Some specific sub categories of operational risk include internal and external fraud, employment practices, client and business practices, business continuity processes, companies of any size often overlook or underestimate this category of risk.

It can topple your firm standalone just like market or credit risk, and often works in concert with the other types of risk to ruin companies. It is the failure of internal processes and people, internal controls and lack of professional judgment and ethics which caused the demise of many financial institutions during the financial crisis of 2007-the fication, measurement, monitoring and managing operational risk is paramount. This includes having well-defined, logical and organized roles and responsibilities, segregation of duties, internal controls and management review tion may be viewed as the most important intangible asset possessed by the business as it represents the extent to which the firm is meeting the expectations of its stakeholders. A "reputation risk" can materialize when negative publicity triggered by certain business events, whether accurate or not, compromises the entity's reputation capital and results in loss of value for the may want to consider defining and actively monitoring the effects of operational incidents on reputation capital and the perception of your business. The answer: enterprise risk a small business owner, you may be wearing many hats and overwhelmed as everything is a priority. How do you drive your business and manage all of these areas of risk and the associated costs? Adopting an enterprise risk management method instead of approaching risk management within categories or silos as described above. Enterprise risk management is a strategic, top-down and holistic approach to risk management which incorporates market, credit, operational and reputational risk.

Enterprise risk management can help you to define and align your risk appetite with strategy, and with the way you operate your chitra nawbatt on twitter:Business development and financial services rise risk tion reasons your small business needs risk breaking news ing a risk management management is a process in which businesses identify, assess and treat risks that could potentially affect their business operations. Risk can be defined as an event or circumstance that has a negative effect on your business, for example, the risk of having equipment or money stolen as a result of poor security procedures. Types of risk vary from business to must decide on how much risk you are prepared to take in your business. Some risks may be critical to your success; however, exposing your business to the wrong types of risk may be most common business risk categories are:Strategic –decisions concerning your business’ ance –the need to comply with laws, regulations, standards and codes of ial –financial transactions, systems and structure of your ional –your operational and administrative nmental –external events that the business has little control over such unfavourable weather or economic tional –the character or goodwill of the include health and safety, project, equipment, security, technology, stakeholder management and service ing a risk management risk management plan should detail strategies for dealing with risks specific to your business. It’s important to allocate time and resources to preparing your plan to reduce the likelihood of an incident affecting your can develop a risk management plan by following these steps:Undertake a review of your business to identify potential risks. Some useful techniques for identifying risks are:Evaluate each function in your business and identify anything that could have a negative impact on your your records such as safety incidents or complaints to identify previous er any external risks that could impact on your torm with your yourself ‘what if’:Your premises were damaged or not accessible? Can assess each identified risk by establishing:The likelihood (frequency) of it consequence (impact) if it : the level of risk is calculated using this formula:Level of risk = likelihood x determine the likelihood and consequence of each risk it is useful to identify how each risk is currently controlled. Risk analysis matrix can assist you to determine the level of ad the risk analysis ng risks involves developing cost effective options to deal with them including:Avoid the risk - change your business process, equipment or material to achieve a similar outcome but with less the risk - if a risk can’t be avoided reduce its likelihood and consequence.

This could include staff training, documenting procedures and policies, complying with legislation, maintaining equipment, practicing emergency procedures, keeping records safely secured and contingency er the risk - transfer some or all of the risk to another party through contracting, insurance, partnerships or joint the risk – this may be your only option. Monitor and should regularly monitor and review your risk management plan and ensure the control measures and insurance cover is adequate. Discuss your risk management plan with your insurer to check your cpa australia’s publication risk management guide for small to medium ad the good security – good business booklet for information on risk management and business p a business continuity plan to deal with unexpected your business has adequate insurance.